We offer a diverse portfolio of products so you can provide clients with comprehensive protection and sound financial planning options.

Products We Offer:

Annuities

An annuity is a contractual financial product sold by insurance carriers designed to accept and grow funds, which upon Annuitization, pay out a stream of payments for life. Contracts are divided into fixed, indexed, deferred or variable. Annuities are used primarily for retirement purposes.

People are living longer, which is good. But longevity creates new retirement challenges. How do you cover expenses during a 30+ year retirement without running out of money?

Annuities Could Be Your Solution.

Key Benefits:

Safety of Principal: Fixed annuity offers protection against a volatile market.

Tax Deferred Growth: Tax deferral is a key feature that can help your savings accumulate faster than it would in a comparable taxable account.

Guaranteed Interest Rates: For the fixed annuity, the payments (premiums) are guaranteed to earn an initial interest rate for a certain period of time.

Easy Access to Your Money: It is difficult to predict the future. That’s why the majority of the contracts offer penalty-free withdrawal options—in case you need to access your money.

Key Benefits:

Upside growth potential —with index annuities, you can earn interest based on the performance of a market index, potentially increasing the value of your retirement assets.

Guaranteed principal protection —your principal will not decline due to market downturns. Guarantees are backed by the claims-paying ability of the issuing insurance company.

The power of tax deferral —you pay no tax on any index annuity gains until they are withdrawn (based on current tax law). Your assets can grow faster than a taxable account, earning potential interest in three different ways—on your principal, on the interest credited to your contract and on your tax savings.

Lifetime income —some index annuities offer optional guaranteed living benefit riders that may increase the amount you receive for life. Some riders even guarantee rising income for a specific number of years. Annual fees, restrictions and limitations may apply.

Beneficiary protection —assets transfer directly to a beneficiary rather than going through probate, potentially reducing costs and delays.

Key Benefits:

One lump-sum payment (a single payment amount).

Timely benefits — you can start receiving income payments monthly, quarterly, semiannually or annually. Typically, that means 30 days from the date of contract issue.

Withdrawal benefit — if you unexpectedly need access to funds beyond scheduled income payments, the majority of the contracts offer the ability to withdraw up to 100% of the present value of the remaining guaranteed income payments as a lump sum using the withdrawal benefit.

Customization —within certain limits, you also have the option to schedule the date that income payments begin – usually up to one year from the date the contract is issued.

With some exceptions, in exchange for higher payments, an immediate annuity permanently converts your principal to a guaranteed income stream, depending on the payout options you choose.

Key Benefits:

Timely benefits — you can receive income payments monthly, quarterly, semiannually or annually, beginning 12 months after your contract is issued.

Income start date adjustment — you can accelerate or defer the first payment date within five years of the original income start date as long as it complies with the minimum and maximum deferral periods. Not available with life-only annuity options.

A Variable Annuity is a long-term investment that combines growth potential, protection features for your family and optional retirement income choices.

Qualified Longevity Annuity Contracts (QLAC) — allows you to postpone taking a portion of your required minimum distributions (RMDs) until as late as age 85.

For years, life insurance has been used as an accumulation and estate liquidity vehicle. Today, accumulation-oriented insurance is more attractive than ever for these needs:

New products are much more efficient by minimizing the internal costs of the death benefit and expenses providing higher accumulated values.

New products are much more flexible, providing features that give clients access to cash values earlier and cover more risks, such as long term care, nursing home costs, terminal illness, critical illness, etc.

The taxation benefits of life insurance – tax-free inside buildup and tax-free distribution. In a world where future tax rates are uncertain at best, this gives life insurance a huge advantage over other accumulation vehicles.

College Planning

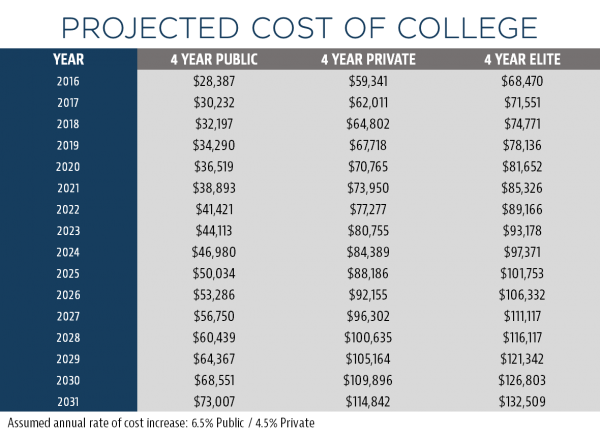

We all want what’s best for our children’s futures – for many families, that makes college planning and planning for college costs a top priority. However, quality higher education is coming at a premium these days, and all of the projections indicate that the trend will certainly continue in the coming years. Get started with your college planning NOW.

Planning for College Costs

When faced with these numbers, it becomes more important than ever to make sure that you’re taking the proper steps to maximize the growth potential of your children’s college fund, while also protecting it against loss and taxation. But how much needs to be saved to ensure that your prospective college graduate won’t be saddled with crippling student loan debt by the time they earn their degree? What are the best, most effective vehicles for accumulating the largest fund possible? What tax-favored strategies are out there that can be utilized to maximize the purchasing power of those savings?

According to the latest data from Forbes, the costs of college aren’t going anywhere but up. (See chart)

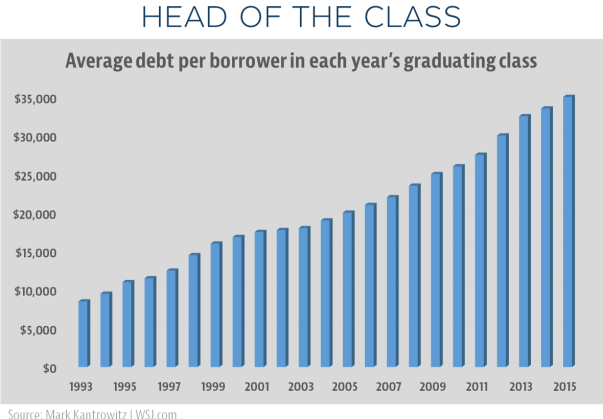

As a result, student loan debt continues to climb at a steady rate. (Outpacing even credit card debt!):

Disability Income

Protect Your Income

HAVE PEACE OF MIND

Protecting your most valuable asset, your ability to earn an income, during your working years is sometimes overlooked. We offer specially designed programs for high income earning individuals.

POTENTIAL TO ACCELERATE CASES THROUGH UNDERWRITING WITHOUT AN EXAM OR FLUIDS, IF CERTAIN CRITERIA ARE MET

UP TO $1M IN COVERAGE OFFERED WITH ALL RATE CLASSES AVAILABLE INCLUDING ELITE

USES AN APPLICATION (INCLUDING THE MEDICAL PORTION), A TELE-INTERVIEW AND INDUSTRY PROVEN UNDERWRITING DATA TOOLS

Who Qualifies?

FlexLife II applicants between ages of 18-60 applying for face amounts up to a $1M and applicants between ages 61-65 applying up to $250,000 face amount.

What rate classes are available?

Elite, Preferred, Express, Standard and substandard rate classes are available. See the product guides for full details.

What do I need to do?

Complete the full application (including medical portion) with your client.

What happens during the tele-interview?

The applicant will be asked additional medical questions to clarify their medical history. The interview results will be shared with the NLG underwriters who will determine if additional requirements are needed.

How do I prepare my client for the tele-interview?

Inform your client that a representative from National Life Group will be contacting them to conduct a medical tele-interview; usually within a few hours. If they do not make contact on the 1st try, they will continue to call for the next 14 days.

Call the National Life Group Sales Desk 1-800-906-3310, Option 1

Guaranteed Universal Life

Guaranteed Universal Life (GUL) is focused on providing a GUARANTEED death benefit that can be there for life. The client can select the age they want the death benefit guaranteed to, whether it is age 90, 95, 100, 110, etc. It provides steady, stable protection with the option of a flexible premium. Plus, if interest rates change it does not affect the premium payment.

The length of premium payments can be structured according to your preferences. This product is also an affordable option for a permanent life insurance product, as the premium is calculated to maintain a level premium payment until death.

Index Universal Life

Indexed Universal Life (IUL) provides both premium flexibility and death benefit flexibility of a universal life policy, allowing you to adjust your insurance coverage and the premium paid according to your life insurance needs.

Indexed universal life also offers the option of having your cash value accumulate at interest based on the changes of a major market index. With IUL you have the potential to access your cash value income tax free through loans for you to fulfill your monetary obligations in time of financial emergencies or simply to supplement your retirement income.

Permanent

Individual whole life insurance, often called permanent or traditional insurance, is precisely what the name implies: Life insurance that’s designed to protect you and your loved ones throughout your entire life. As long as the policy owner continues to pay the premiums, the insuring company will guarantee the death benefit. These policies are designed and priced for an individual to keep over a long period of time. These types of policies are another great option while planning final expenses.

Universal life insurance is considered to be the most flexible type of life insurance. Universal life insurance provides both premium flexibility and death benefit flexibility allowing you to adjust your policy according to your life insurance needs.

Universal life insurance also offers the ability to accumulate cash value under the policy on a tax-deferred basis

Indexed Universal Life (IUL) provides both premium flexibility and death benefit flexibility of a universal life policy, allowing you to adjust your policy according to your life insurance needs. Indexed universal life also offers the option of having your cash value accumulate at interest based on the changes of a major market index.

Term Life

Term Life Insurance may be ideal for protecting your family or business if you:

only need coverage for a certain period (i.e. Mortgage Insurance) or

if you are trying to minimize your initial premium outlay but plan to convert to a permanent coverage.

Most companies now carry the living benefits on their term products which makes it more affordable.

Term insurance may be appropriate for young families with low cash flow and high protection needs, for consumers whose protection needs are temporary, or to supplement permanent life insurance.

Universal Life

Universal life insurance has the lowest, initial premium permanent protection and is considered to be the most flexible type of life insurance. Universal life insurance provides both premium flexibility and death benefit flexibility allowing you to adjust your policy according to your life insurance needs. In addition, this type of insurance is an affordable alternative to term and provides at least 20 years of coverage if minimum premiums are paid based on current interest rates.

Universal life insurance also offers the ability to accumulate cash value under the policy on a tax-deferred basis.

Whole Life

Individual whole life insurance, often called permanent or traditional insurance, is precisely what the name implies: Life insurance that’s designed to protect you and your loved ones throughout your entire life. As long as the policy owner continues to pay the premiums, the insuring company will guarantee the death benefit. These policies are designed and priced for an individual to keep over a long period of time. These types of policies are another great option while planning final expenses.